Friends,

I find it interesting that the information below comes at a time when we have

just had our second Blood Moon on 8 October. We have also just begun the

Shemittah year and Obama awaits his personal harbinger for writing "We remember We re-build, we come back stronger!" on a girder for the new Freedom Tower.

On 20 March 2015 we will have a solar eclipse. A solar ecipse is a warning to the world, while the Blood Moons are a warning to the Jews and the nation of Israel. In 2016 the

Palestinians want the UN to declare a Palestinian state – a two state solution

and in 2017 Israel has a jubilee.

HOW WE LOOKIN, NOT GOOD! If you are on the fence concerning Yeshua Hamashiach/Jesus Christ, now is the time to believe in Him and repent of your sins. Our redemption is drawing nigh.

HOW WE LOOKIN, NOT GOOD! If you are on the fence concerning Yeshua Hamashiach/Jesus Christ, now is the time to believe in Him and repent of your sins. Our redemption is drawing nigh.

A nation where the top 10 percent reaps more than 50 percent of the income is doomed to end up in the quicksand of deflation, dragging down the rich along with everyone else. The Federal Reserve’s timidity to address this reality since the crisis of 2008, as the national debt ballooned and its own balance sheet quadrupled, has now put it in a dire pickle at a most inopportune time.

The Fed has attempted to assure the world that things are so dandy here in the “Goldilocks economy” that its biggest focus is when it will raise interest rates to keep the economy from overheating and keep inflation in check. That thesis has been quite a bit of a stretch with 45.3 million of its fellow citizens living in poverty and a labor force participation rate of 62.7 percent – a data point that has been steadily getting worse since the financial crisis in 2008.

A key component that has allowed both the Fed and Congress to keep from taking strong measures to address a looming deflation has been the price of crude oil. Because oil impacts everything from transportation costs that inflate the price of food and other products to the cost of an airline ticket or heating a home, the high price of this commodity has, to a degree, masked the growing deflation threat.

Now the mask has been removed. Oil prices are in freefall and an oil price war has broken out among OPEC members, raising the specter of 1986 when oil prices fell by 50 percent in just an eight month span. A serious global slowdown has effectively turned the oil cartel, OPEC, into a beggar thy neighbor band of go-it-alone dealmakers who hope to sign individual contracts with customers and grab market share before prices decline further.

Earlier this month, Saudi Arabia’s state-owned oil company, Saudi Aramco, cut its official crude price by $1 a barrel for November deliveries to its Asian customers. It also dropped pricing by approximately 40 cents a barrel to U.S. and European customers. According to OPEC data, “Saudi Arabia possesses 18 per cent of the world’s proven petroleum reserves and ranks as the largest exporter of petroleum.” As the world learned in 1986, if Saudi Arabia wants to start a price war to assert its dominance, it has both the resources and production capability on its side.

According to a report from Bloomberg News, Iran is now offering oil discounts similar to Saudi Arabia. The situation is fraying nerves in countries dependent on oil revenues with Venezuela calling for an emergency OPEC meeting prior to its regular meeting slated for November 27.

Before the latest news of OPEC’s disarray sent oil prices plunging, the Fed was already expressing some concerns about the low rate of inflation. Its minutes for the Federal Open Market Committee (FOMC) meeting of September 16 – 17, 2014 included the following:

“Total U.S. consumer price inflation, as measured by the PCE [Personal Consumption Expenditures] price index, was about 1½ percent over the 12 months ending in July. Over the 12 months ending in August, the consumer price index (CPI) rose about 1¾ percent…

“The staff continued to project inflation to be lower in the second half of this year than in the first half and to remain below the Committee’s longer-run objective of 2 percent over the next few years. With longer-term inflation expectations assumed to remain stable, resource slack projected to diminish slowly, and changes in commodity and import prices expected to be subdued, inflation was projected to rise gradually and to reach the Committee’s objective in the longer run.”

In other words, a sudden, sharp drop in inflation expectations caused by an oil price war raging around the globe was not present in the Fed’s crystal ball just a month ago. But it should have been: other commodity prices have been sending up red flags for some time now. On September 24, just one week after the Fed’s September meeting:

“Iron ore has now slumped 41 percent this year, marking a five-year low. In just the third quarter the price is off by 15 percent, suggesting the trend remains in place. This week the price broke $80 a dry ton for the first time since 2009.

“Agricultural commodity prices are also confirming the trend with corn off 22 percent since June and wheat down 16 percent in the same period. Soybean prices are down 28 percent this year to the lowest in four years.

“Deflationary winds blowing in from Europe, cooling economic growth in China, together with the question of just how disfigured the stock market has become as a result of $1.09 trillion propping up the S&P 500 through corporate buybacks in the last 18 months, all signal one word for the average investor: caution.”

Another key gauge of inflation expectations, the 10-year U.S. Treasury note, has been telling the market for some time that deflation was far greater a worry than inflation and that the Fed’s thesis of hiking interest rates next year had all the staying-power of a snow cone in July.

The 52-week high in the yield of the 10-year Treasury note was 3.06 percent. This morning, it is yielding 2.28 percent. That’s not the behavior of an interest-rate benchmark anticipating heated economic growth in the U.S. or an interest rate hike by the Fed.

The market has delivered epiphanies to the Fed on multiple fronts – some of them blazing with sirens – but the Fed seems to have had its head in the sand just as securely as it did heading into the 2008 crisis.

The problem for the Fed, which has already quadrupled its balance sheet to over $4 trillion to sustain a less than 2 percent inflation rate while keeping interest rates in the zero-bound range, is that its monetary arsenal loses its firing power with the onset of deflation, should it occur.

Deflation boosts the value of holding cash and deferring purchases. The thinking goes like this: the longer you wait to buy, the cheaper the house or product becomes, effectively raising the value of the cash you hold. Conversely, if you spend your cash prematurely, the product or investment you buy may lose future value as a result of the deflation, handing you a wealth loss. If enough people adopt that attitude and defer enough purchases, the deflationary spiral becomes self-reinforcing, as it did in the Great Depression.

Then there is the problem of the strong U.S. dollar. This hampers export growth for U.S. manufacturers because it costs more in local currencies to buy the product we are attempting to sell in foreign markets. A strong dollar can also accelerate deflationary trends by making foreign imports cheaper in the U.S. as a result of the increased purchasing power of our currency. This would further complicate the Fed’s ability to beat deflationary forces.

As Wall Street on Parade reported in December, the Fed prides itself on gathering intelligence from the marketplace, starting its day at 4:30 a.m. at the New York Fed and ending up around 6:30 p.m. with conference calls to the Federal Reserve Board of Governors in between. The growing fear is that the Fed is once again, like 2008, watching the market tick by tick but failing to see the larger, dangerous trends.

Only

two weeks into the new Shemitah year of 2014-2015, the U.S. stock market has

already shed hundreds of points.

Theresa Yarosh, founder and president of Macro Wealth Management LLC in Paramus, New Jersey, said she has reviewed the accuracy of the patterns laid out in Cahn’s book, “The Mystery of the Shemitah.”

“It is accurate based on underlying market patterns and economics,” Yarosh said. “I traced the pattern all the way back to 1916. Jonathan had the question as to why some of the (seven-year) cycles are more powerful than others and that’s because you have to apply the debt cycle and some (Shemitahs) have more debt to be worked out than others.”

She said the financial meltdowns of 2001 and 2008, as bad as they were, did not fully correct the debt bubbles that had built up.

“Now we’re in another one. Where his book is strong is in the (Shemitah’s) need for a full release of the debts. The last two recessions did not correct that,” Yarosh said.

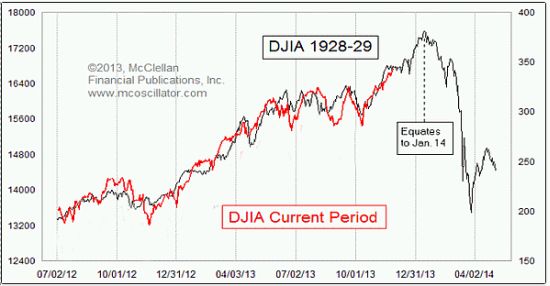

Similarities to 1930s Depression

Yarosh sees a debt cycle peak being built up similar to that of 1933. The initial market crash occurred in 1929 and then came the deleveraging of the 1930s with a secondary downturn in the market in 1938.

That’s when the financial reckoning was completed.

“The period we’re in now is almost like the Roaring Twenties with a build up of enormous margin debt,” Yarosh said. “My advice would be to balance out things that have guarantees with things that don’t. It’s like the story of the tortoise and the hare. Slow and steady wins the race with a focus on risk management.”

Because of the conservative economic model Yarosh works with, she is not concerned with where the market is headed.

“I have clients that have a lot of cash, who are very liquid,” she said. “So, I would say, have sufficient liquidity, at least three to six months of living expenses in cash, and about 50 percent of your gross income should be liquid. That’s a high amount of liquidity. Most investors don’t have that.”

Billionaires investors like Warren Buffet, Marc Faber, Donald Trump, Peter Schiff and others have all made statements recently that they see a major market correction coming and that it could be worse than 2008. Faber warns of “massive wealth destruction” coming to America in which he predicts “well-to-do people will lose up to 50 percent of their wealth.”

Yarosh sees another troubling sign that smaller investors might want to pay attention to: The ultra wealthy are hording cash.

According to the new Billionaire Census from Wealth-X and UBS, the world’s billionaires are holding an average of $600 million in cash — greater than the gross domestic product of Dominica. That marks a jump of $60 million from a year ago and translates into billionaires’ holding an average of 19 percent of their net worth in cash. This increased liquidity signals that many billionaires are keeping their money on the sidelines and waiting for the optimal moment to make further investments.

“These are people who know what’s going on, who see things on a very big level, and it’s not good,” Yarosh said.

Yarosh said she has studied economics and economic patterns for more than 20 years but Cahn’s research has shed light on a lot of questions.

“There has always been something to the ‘autumn phenomenon,’” she said, referring to the long-held suspicion among investors that crashes tend to happen in September and October. “And people for years have wondered why that is. I think Jonathan has tied it to the Hebrew calendar and the Bible.”

Signs of things to come for U.S. economy?

Cahn said that the loss of more than 260 points in the Dow Jones Industrials on the very first day of the Shemitah year could be the “first fruits” of more market mayhem over the next 12 months. The market lost another 449 points over a two-day period, Oct. 9-10, coinciding with the opening of the Jewish Feast of Tabernacles.

But the shakings brought on by the Shemitah are not limited to the financial realm.

Theresa Yarosh, founder and president of Macro Wealth Management LLC in Paramus, New Jersey, said she has reviewed the accuracy of the patterns laid out in Cahn’s book, “The Mystery of the Shemitah.”

“It is accurate based on underlying market patterns and economics,” Yarosh said. “I traced the pattern all the way back to 1916. Jonathan had the question as to why some of the (seven-year) cycles are more powerful than others and that’s because you have to apply the debt cycle and some (Shemitahs) have more debt to be worked out than others.”

She said the financial meltdowns of 2001 and 2008, as bad as they were, did not fully correct the debt bubbles that had built up.

“Now we’re in another one. Where his book is strong is in the (Shemitah’s) need for a full release of the debts. The last two recessions did not correct that,” Yarosh said.

Similarities to 1930s Depression

Yarosh sees a debt cycle peak being built up similar to that of 1933. The initial market crash occurred in 1929 and then came the deleveraging of the 1930s with a secondary downturn in the market in 1938.

That’s when the financial reckoning was completed.

“The period we’re in now is almost like the Roaring Twenties with a build up of enormous margin debt,” Yarosh said. “My advice would be to balance out things that have guarantees with things that don’t. It’s like the story of the tortoise and the hare. Slow and steady wins the race with a focus on risk management.”

Because of the conservative economic model Yarosh works with, she is not concerned with where the market is headed.

“I have clients that have a lot of cash, who are very liquid,” she said. “So, I would say, have sufficient liquidity, at least three to six months of living expenses in cash, and about 50 percent of your gross income should be liquid. That’s a high amount of liquidity. Most investors don’t have that.”

Billionaires investors like Warren Buffet, Marc Faber, Donald Trump, Peter Schiff and others have all made statements recently that they see a major market correction coming and that it could be worse than 2008. Faber warns of “massive wealth destruction” coming to America in which he predicts “well-to-do people will lose up to 50 percent of their wealth.”

Yarosh sees another troubling sign that smaller investors might want to pay attention to: The ultra wealthy are hording cash.

According to the new Billionaire Census from Wealth-X and UBS, the world’s billionaires are holding an average of $600 million in cash — greater than the gross domestic product of Dominica. That marks a jump of $60 million from a year ago and translates into billionaires’ holding an average of 19 percent of their net worth in cash. This increased liquidity signals that many billionaires are keeping their money on the sidelines and waiting for the optimal moment to make further investments.

“These are people who know what’s going on, who see things on a very big level, and it’s not good,” Yarosh said.

Yarosh said she has studied economics and economic patterns for more than 20 years but Cahn’s research has shed light on a lot of questions.

“There has always been something to the ‘autumn phenomenon,’” she said, referring to the long-held suspicion among investors that crashes tend to happen in September and October. “And people for years have wondered why that is. I think Jonathan has tied it to the Hebrew calendar and the Bible.”

Signs of things to come for U.S. economy?

Cahn said that the loss of more than 260 points in the Dow Jones Industrials on the very first day of the Shemitah year could be the “first fruits” of more market mayhem over the next 12 months. The market lost another 449 points over a two-day period, Oct. 9-10, coinciding with the opening of the Jewish Feast of Tabernacles.

But the shakings brought on by the Shemitah are not limited to the financial realm.

On the first day of the Shemitah year, Sept. 25, the first case of Ebola was diagnosed on U.S. soil, when Thomas Eric Duncan checked into a hospital in Dallas, Texas. Duncan died on Oct. 8, the day that a blood moon appeared in the sky, the second of a rare series of four lunar eclipses that will occur on Jewish High Holy Days between autumn of 2014 and autumn of 2015.

Cahn has pointed that, according to his research, the worst of the worst usually happens at the end of the Shemitah year, not at the beginning. In fact, the last day of the year, Elul 29 on the Hebrew calendar, which will occur on Sept. 13, 2015, is the most dreaded day.

The pattern revealed in “The Mystery of the Shemitah” is that the beginning of the Shemitah’s impact is often subtle, but leads to a dramatic climax.

“The beginning may mark a change in direction, even a foreshadow of what will come to a crescendo at the Shemitah’s end,” he said.

In the Shemitah of 2000-20001, the beginning marked a sudden downturn of production. Its culmination came in the second week of September, 2001, the week that saw the calamity of 9/11 and the greatest stock market collapse in history to that date.

In the Shemitah of 2007-2008, it’s beginning saw a stock market that had been rising for years, suddenly reverse course and begin to descend. The culmination came in September 2008 with the global financial implosion, the collapse of Wall Street on Elul 29 on the Hebrew calendar, marking the greatest one day crash in stock market history, followed by the Great Recession.

“In the book I’ve marked out the Shemitah’s beginning – and many were watching to see if anything significant would take place,” Cahn said. “What happened with this Shemitah was even more dramatic than in the past. Within two days of the Shemitah’s start, the stock market began to descend. On the Shemitah’s very first day, Wall Street plunged over 260 points. It was the event that marked the beginning.

No comments:

Post a Comment